Hello Visitor! Log In

The World Will Never be the Same: The Russia-Ukraine Conflict as a Trigger Point for Deglobalisation

ARTICLE | June 20, 2022 | BY Patrick Liedtke

Author(s)

Patrick Liedtke

Get Full Text in PDF

Get Full Text in PDFAbstract

This paper makes the case for why we believe that the Russia-Ukraine crisis signals the end of a global era defined by globalisation. Even though Russia’s economy is only a fraction of the US, EU or China, its role in the world is much more relevant and the events in Ukraine are triggering a cascade of effects that will redefine the political, social and economic thinking and interactions among nations long into the future. With the Russian invasion of Ukraine, the “peace dividend” of recent decades is gone as military budgets are increasing significantly around the world. Energy and raw material dependency on other countries is considered a strategic weakness. The war has disrupted global supply chains and nations are now shunning the exposure to other countries, especially ones that do not share similar values. The macroeconomic environment has changed as growth prospects are depressed and inflation is on the rise. The world is moving to a period of reorganisation and instability.

1. Preamble: Thoughts for the people affected by the conflict in Ukraine

Before discussing mostly economic aspects that the Russia-Ukraine conflict has triggered, we would like to emphasize that no financial consideration and economic discussion should let us forget that this conflict has seen human suffering on a scale that Europe had been previously spared for a long time.

We want to express our deepest sympathies with everybody who has been drawn into this conflict and suffers because of it. Our thoughts are with the many civilians and soldiers who have lost their lives and their family and friends, with the victims who have been hurt, the people who had their homes and livelihoods destroyed, and with the refugees who had to flee their homes.

2. Introduction

Geopolitical events come and go. And while wars are human tragedies, unless they affect major economies their effects on financial markets and the enveloping economic eco-system are usually limited and transient. The historic databanks are full of examples of how stock and bond markets recover after an initial shock. Sometimes this takes longer, but the conventional wisdom is that unless there is a major and lasting disruption to the world economic system, the world will keep turning and finance will move on.

In this paper, we will make the case for why we believe that the Russia-Ukraine crisis is different. It is different for several reasons. Even though Russia’s economy is only a fraction of the US, EU or China, its role in the world is much more relevant than this. In the GDP ranking of nations, Russia only occupied the 12th spot in 2019 with a GDP according to the IMF of USD 1.67trn. To compare, this is one spot above Spain and four below Italy. And Ukraine figures in 57th position, with a GDP of USD 147bn.*

"It is not the Russian war in Ukraine that causes the future to be different. It is a different future that begins with the Russian war as the first major event of a new era."

Qualifying the conflict as having only limited impact purely because the GDP of the nations involved is small compared to the rest of the world, neglects the role of Russia as an important producer of energy, in particular fossil fuels, and of commodities, especially metals and uranium. We shall analyse the latter in more detail, but even though Russia is a top producer of many raw materials, our reasons for why this crisis will have longer lasting effects lie elsewhere.

The Russian crisis is an inflection point at the end of an era. For several decades, the world moved ever closer and globalisation brought unprecedented growth and prosperity to many parts of the world. Lasting peace allowed many nations to reap a “peace dividend” in the form of lower military spending, which allowed more investments elsewhere. However, a few years ago this trend started to slowly reverse.

As the Russian bombs are bringing devastation to a European country, several things suddenly become more apparent: First, with an unprovoked attack by one of the leading military forces in the world on a neighbouring nation, the premise of global (relative) peace, at least among the larger nations, no longer holds. The world is reacting to the Russian violation of Ukraine’s territorial sovereignty by rearming itself. The peace dividend is gone.

Second, the energy and raw material dependency on Russia has created a deeper rethink about sourcing and supplying in the future. While Europe is at the forefront of changing its procurement systems, particularly sensitive given its high dependency on Russia, it is not alone. Other nations are reconsidering how far they should have concentration risks in their economic production system and are keen on reducing them.

Third, while the COVID-19 pandemic already led to nations becoming more occupied with themselves, the war has disrupted global supply chains to a larger extent than the GDP-weighting of Russia or Ukraine would suggest. Nations are now shunning the exposure to countries that do not share similar values and have government systems that are different from their own. While during the period of accelerated globalisation the thinking was that closer interconnectedness would lead to change and transform autocratic governments into democratic ones, Russia has demonstrated that this is a fallacy. As Russia attacked Ukraine, the world looked at China and Taiwan with trepidation.

And finally, the world is waking up to a new macroeconomic environment. The long period of ever lower interest rates and tame inflation is truly behind us. Many countries will see inflation in 2022 like they have not experienced in the working lives of many of their adult population. According to the IMF, the annual inflation rate in the US accelerated to 7.9% in February 2022, the highest since January 1982. And Europe and other leading nations are likely to experience worse. As inflation is on the rise, the future growth prospects are falling. The world is likely to move from a period of relatively constant growth, that not even the Global Financial Crisis and the COVID-19 pandemic could derail for long, to a period of reorganisation where growth will be very uneven and overall lower.

It is not the Russian war in Ukraine that causes the future to be different. It is a different future that begins with the Russian war as the first major event of a new era.

3. Geopolitical Situation

3.1. The slow but steady depart from globalisation

For the better part of the past 75 years, the world moved gradually towards closer interconnectedness. Modern infrastructure, especially transport and communications, made it possible to create supply chains stretching tens of thousands of miles across the world. They facilitated the growing exchange of information, investments, goods and services on a world-wide scale. Globalization became the term used to describe not only this exchange but the resulting growing interdependence of the world’s economies, cultures, and populations.

The creation and then steady expansion of what is today the European Union, the establishment of the North American Free Trade Agreement (NAFTA), the Asia-Pacific Economic Cooperation (APEC), and finally the World Trade Organisation were important milestones towards more globalisation. Seminal events like the fall of the Iron Curtain, the rise of the Asian Tiger economies and particularly the accession of China to the WTO exemplified the movement towards increasingly closer (esp. economic) relationships amongst nations.

However, that trend slowly started to lose its impetus and began to even reverse upon itself. While world trade as percentage of GDP† increased from 25% in 1970 to 61% in 2008, it then started to decline, falling to 51.6% in 2020.‡ Foreign direct investments (FDI), another indicator of world interconnectedness that had grown for a long time,§ fell to USD 1.5trn in 2019 (the last year before the pandemic), thus being much lower than the USD 2.7trn in 2016 or indeed the peak of USD 3.1trn in 2007.

Seminal events in recent years that underline the new movement towards deglobalisation include: the shift in US foreign policy (especially vis-à-vis China), Brexit (the first major reversal of the European integration trend since World War II), a reconsideration of far-reaching production chains under climate change considerations, as well as the often very nationalistic and protectionist response to the COVID-19 pandemic (incl. independent and uncoordinated measures to contain transmission, limitations to global vaccine distribution, arbitrary travel restrictions etc.).

With the Russian-Ukrainian conflict, two things have happened very quickly. Firstly, the previously rather overlooked movement towards de-globalisation has received a massive boost and is now more widely recognised. And secondly, next to the prior mostly economic and financial considerations regarding supply change organisation, another dimension came to the fore: the increased vulnerability to political events and military operations. The latter has led, in turn, to a reconsideration of national attitudes towards countries that do not form part of the same economic and military alliance.

3.2. The Russian invasion of Ukraine as a trigger point

When the Russian tanks started rolling into Ukraine, it was not merely the start of a local military operation but became the cause for a series of widespread and cascading reactions by many countries opposing the invasion. These in turn led to several rounds of retaliatory responses amongst the involved nations and their allies. First and foremost, there is the military dimension: all aspects directly relating to the ongoing war in Ukraine, from military procurement to battlefield action and strategic military planning. The conflict has triggered a rethinking regarding security needs by many nations, not just those directly involved in the conflict but practically the world over.¶

Second are the very significant geopolitical consequences. Immediately following the Russian invasion of Ukraine, security experts around the world began to not only wonder about possible other Russian threats but grew particularly worried about other non-democratic regimes, especially China.** In the meantime, discussions on NATO enlargement through membership of Finland and Sweden—two countries who since World War II have pursued a policy of neutrality—are gathering traction.††

And thirdly, the avalanche of economic and financial measures that was unleashed by and upon the world, such as the introduction of sanctions and embargoes by the US, the EU, Ukraine, Russia and many of their respective allies, is having widespread impact.‡‡

However, as the conflict unfolded, it became clear very quickly that its ramifications would not be limited to the military, geostrategic and economic dimensions, but be far more pervasive. The exclusion of Russia from international bodies (ranging from the economic and financial like the Swift payment system to the cultural like sporting events), the introduction of travel bans, operational restrictions, asset freezes and seizures have unravelled also cultural and social ties that previously had existed for many decades. Suddenly the world is clearly headed in a new direction.

3.3. The renaissance of national and regional independence and autonomy

After the Second World War, the Allied nations that had fought fascist Germany and Italy in Europe and imperial Japan in Asia came to the realisation that a repeat of the punitive policies following World War I was not the best approach to create lasting peace and stability. Instead, they aimed at reforming political and social structures in the countries that had lost the war, pursuing a strategy where closer financial links, economic cooperation and social interaction would make a war less likely. This plan was hugely successful in Europe and Japan, sparking the creation of the European Common Market (later the European Union) while in Asia, Japan became an important partner to the US and Europe.

This valuable lesson was not lost on the Europeans and as the old Soviet Union disintegrated, the European Union, led by Germany as the driving force, adopted in the 1990s a similar policy towards Russia. German Chancellor Gerhard Schröder coined the phrase “Wandel durch Handel”, i.e. “Change through trade”, trying to pull Russia closer towards Europe by creating close economic ties and making Germany consciously gradually more dependent on Russian commodities, especially oil and gas. Other European nations followed.§§ The idea was again to avoid conflict through closer interconnectedness and mutual dependency.

The wisdom of this idea with regard to Russia is now being called into question. The European Commission announced on 8 March 2022 that it “…has today proposed an outline of a plan to make Europe independent from Russian fossil fuels well before 2030, starting with gas, in light of Russia’s invasion of Ukraine.”¶¶ The wider conclusion now drawn is that closer economic and financial connectedness, especially without deeper social and political reforms, are apparently not enough to prevent military conflict.

And this lesson is being applied not only to Russia or Belarus by Western nations but also reshaping the position towards China and other nations. Back in 2009, the European Parliament wrote that it “…believes that democracy requires an effective civil society, which is in turn strengthened by trade and economic relations with the European Union; therefore believes that ‘change through trade’ is a way to aid China’s transformation towards being an open and democratic society benefiting all sections of society”.*** Since then, the European Union has been more guarded regarding those ambitions while the US already engaged in a trade war with China in 2017††† and wondered openly following Russia’s attack about China’s intentions regarding Taiwan.

So, while a general and fundamental reappraisal of the risks inherent in international trade and the dependency of a nation’s production systems on other countries is being undertaken, the driving force of globalisation has turned into the contrary and the ideological paradigm of “change through trade” is replaced by a desire for more independence and greater autonomy.

4. Economic and Social Consequences

4.1. International dependency on Russian primary goods

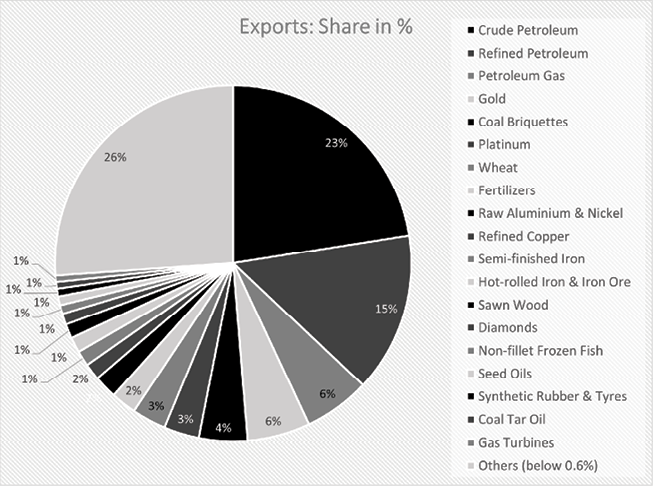

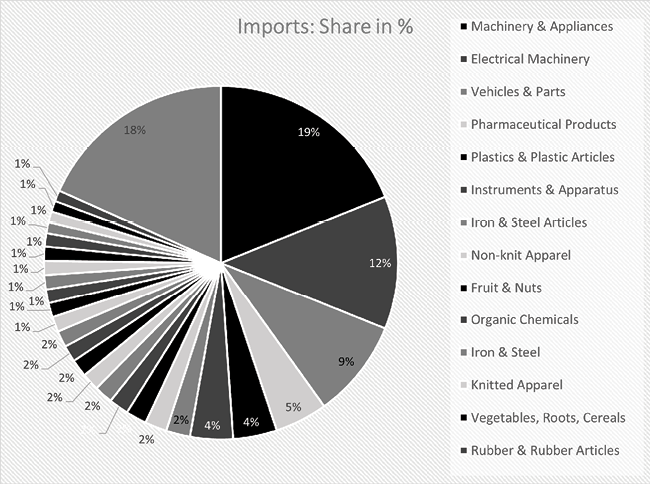

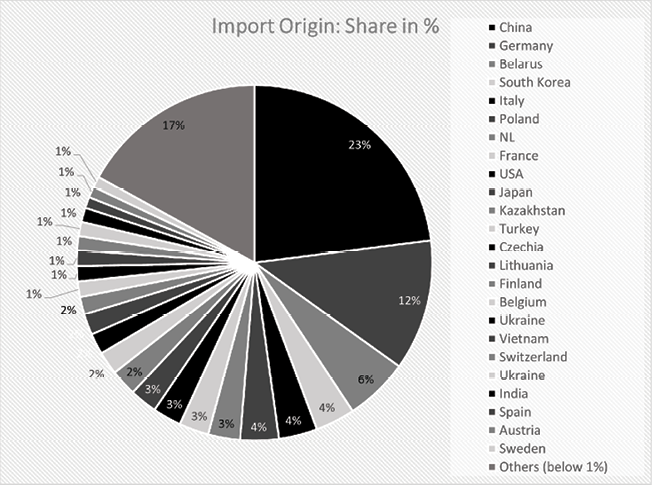

According to the World Bank, the Russian Federation had total exports of USD 427bn and total imports of 247bn.‡‡‡ The GDP of Russia in 2019 was USD 1.69trn. The Federation’s exports of goods and services as percentage of GDP amounted to 28.54% and imports of goods and services as percentage of GDP was 20.91%.

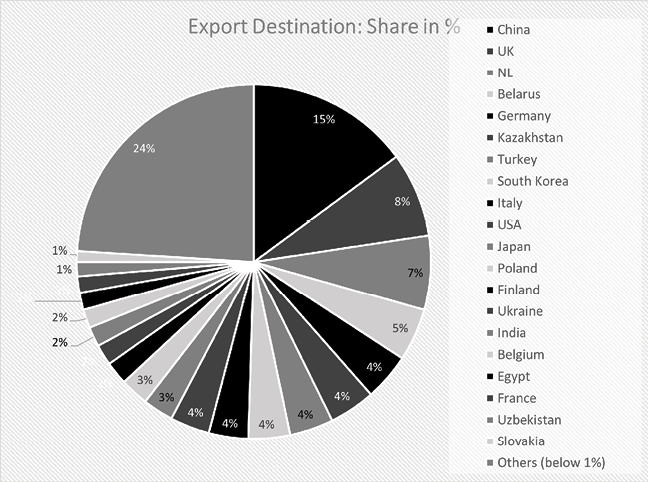

A visualisation of Russia’s export and import data is shown below.§§§

With a positive trade balance of USD 180bn and a fairly limited value of imports (at least in proportion of the overall GDP), the Russian economy is not as dependent on foreign goods as many other open economies. However, its exports are highly concentrated and consist of predominantly fossil fuels and metals, which together make up about two thirds of all exports.

| Country | Share of Russian oil* | Share of Russian gas |

|---|---|---|

| Finland | 100% | 67.80% |

| Netherlands | 100% | 35.90% |

| Greece | 90.90% | 38.90% |

| Poland | 76.10% | 46.40% |

| Hungary | 59.20% | 100% |

| Germany | 37.20% | 45.70% |

| Sweden | 33.10% | 14.10% |

| Italy | 18.70% | 40.90% |

| United Kingdom | 16.90% | 3.00% |

| France | 16.70% | 20.00% |

From a strategic point of view, the EU countries are highly vulnerable to an interruption of Russian oil and gas deliveries. The International Energy Agency provides the ratio of Russian imports to domestic fuel consumption in 2020 as in the inset table.¶¶¶

While the US is one of the top 10 destinations of Russian fossil fuels in absolute terms, those make up only a very small part of the US energy needs and can readily be covered domestically or by other producers. For the UK, it is somewhat harder to replace Russian oil (especially diesel) than Russian gas, but its dependency is also far lower than that of the EU. This explains, at least in part, why the US and the UK were quick to ban Russian fossil fuels whereas the EU has been playing for time, particularly to get out of the all-important heating season in Central Europe.

Other sectors are important too: The Food and Agriculture Organization’s Corporate Statistical Database lists Russia as the top exporting nation for grain in 2020. In 2019, Russia was also the 2nd worldwide producer of platinum, 2nd largest world producer of cobalt, 2nd worldwide producer of vanadium, 3rd largest world producer of gold, 3rd largest world producer of nickel, 3rd largest world producer of sulphur, 4th worldwide producer of silver, 4th largest world producer of phosphate, 5th largest world producer of iron ore, and 6th largest producer of uranium (2018).****

According to Trade Data Monitor, Russia was the world’s leading exporter of fertilizers. In 2021, it shipped out USD 12.5 billion worth of fertilizers, up 78.4% from 2020.††††

In summary, the world is having a hard time replacing Russian exports but is feverishly trying to do so.

4.2. Disruption of supply chains and their reorganisation

As the Russian war in Ukraine is having a direct impact on certain supply chains, it is also calling into question whether long and complex sourcing arrangements spanning the globe are indeed the best way forward. For many years, supply chain managers tried to optimise cost as their number one priority, often at the expense of resilience. This changed somewhat, albeit only gradually, with the slowing of globalisation, but it became a hot topic when the Ever Given, a huge super-container ship, ran aground and blocked the Suez Canal in March 2021.‡‡‡‡ Suddenly, global supply chains looked not cheap but vulnerable.

However, the Russian attack has also triggered a more fundamental and holistic reconsideration as the world’s largest country is being perceived as unfriendly and unreliable by many nations.§§§§ At the same time, more questions are being asked about the relationship of the Western democracies with China. An important part of the answer seems to be near-shoring or on-shoring of production systems, thus curbing the reliance on other nations, particularly those that do not share democratic systems, free speech, human rights etc.

In a world where alliances are being redefined stricter along lines of differing philosophies of governance and control, supply chains are likely to follow those lines closer than in the past.

4.3. The ESG dimension

Wars are human disasters of the biggest kind. However, any war is also a catastrophe from an ESG perspective, with massively negative consequences for the environment. Just consider the CO2 emissions of armies, the impact of first destroying and then rebuilding the infrastructure after the conflict, the pollution from ammunition and war materials etc.

Nevertheless, longer-term there might be a silver lining for the global environment and the ESG movement. The important shift away from long supply chains will reduce transport emissions in the future. Shorter supply chains require less energy and create consequently lower emissions. In addition, as more supply chains end in countries with high environmental standards, such as the EU and the US, than in those with lower standards, such as e.g. China or Russia, basing more production in such ESG-orientated countries should further reduce greenhouse emissions and avoid other adverse environmental impacts.

While there are currently discussions underway, especially in Europe, to counter the reliance on Russian oil and gas by burning more of the dirtier coal, these solutions are largely meant to overcome a short impasse. In the long term, the most promising solution is to curb the dependency on fossil fuels for transportation and heating and replace it with renewable energy. For many years, politicians in the EU have strongly advocated for a move towards greener energy and a lower dependency on external energy provision.¶¶¶¶ This position has been recently reinforced as renewables are seen, too, as a solution to the Russian energy crisis. EU Energy Commissioner Kadri Simson said, “…ultimately, the best and the only lasting solution is the Green Deal—boosting renewables and energy efficiency as fast as technically possible. We are still far too dependent on fossil-fuel imports; but boosting home-grown renewables help us out of this trap.”*****

4.4. Economic Demands of the Future

4.4.1. Energy

In the previous sections, we looked at the longer-term consequences of the war in Ukraine and how particularly Europe is in dire straits to find workable solutions. As many countries are keen on replacing Russia as a key energy provider, the regional energy infrastructure will have to change to accommodate this goal. Firstly, short-term alternatives have to be found to replace Russian oil and gas. It is expected that nuclear energy production will play a more prominent role, as already announced e.g. by France and the UK.††††† Other countries like Germany that have tried to avoid it on the grounds of the dangers of its production and the unresolved storage problem of nuclear waste will find it harder to reverse their policy of shutting down nuclear power plants, but the pressure to bring them online again will mount as other alternatives are expensive and slower to build. Dirtier technologies such as an extension of coal burning in Europe are very likely only a brief stop-gap measure while the systems are adapting to the current supply shock.

In the longer term, the expected winners of the energy transformation are widely expected to be renewable power sources, especially those that also work well in countries with colder climates. Oil and gas shall increasingly be replaced by hydropower, wind farms, bioenergy, solar power or geothermal energy, a development for which there is now an even stronger incentive than before.

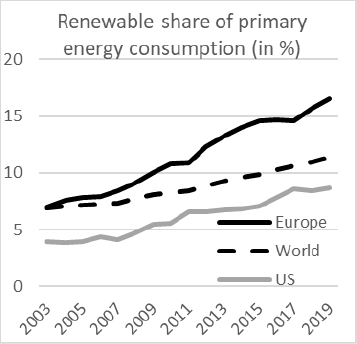

Already over the past years, the worldwide energy production mix has moved towards renewables. In Europe it already comprises 16.5% of total primary energy consumption. While many countries are actively changing their energy mix, this has a direct impact on the energy infrastructure. Instead of Russian gas pipelines, Europe will need a more powerful electrical distribution grid, especially as the production of renewable energy takes place in different locations to where the existing power plants are. Those locations will have to be connected to the grid and the grid made more intelligent. Countries in other parts of the world will take notice of the solutions adopted and likely emulate them.

Besides the supply of energy, alternative forms of flexibility for the power system have to be scaled up as well, notably seasonal flexibility but also demand shifting and peak shaving. Governments, particularly in Europe, need to step up efforts to develop and deploy sustainable and cost-effective ways to manage the flexibility needs of the power systems. A range of options will have to be explored, including intelligent grids, more energy efficiency and increased electrification (esp. instead of direct gas use). In addition to demand-side responses, long-term energy storage technologies have to be deployed alongside short-term sources of flexibility such as batteries or pump stations.

Europe also needs to ensure that there is adequate regulatory support to accelerate the business case for these investments.

4.4.2. IT and Communication

The biggest change in the use of IT and communication technologies in the past decade has been the adoption of work-from-home practices as required by the lockdown restrictions introduced in the wake of the COVID-19 pandemic. Suddenly, with the exception of essential jobs, entire countries started to produce mainly services but also a few goods from home. The existing IT and communications infrastructures were put to a collective stress test.

While the outcome from a business continuation perspective has been largely a success, some shortcomings have become apparent as well. Abundant residential bandwidth and ubiquitous connectivity are still elusive more than 2 years since the first lockdowns, even in the most advanced economies. The reliability of systems is not high enough while data transmission and storage demands shall grow faster than in the past. In this area, further investments will be required as most office workers are expected to mix limited office presence with more productivity at home as part of their normal job routine. Already, several institutions, such as the International Energy Agency (IEA), have called for the establishment of a routine 3-day work-from-home/2-day office presence arrangement to save energy.‡‡‡‡‡

The Russian war in Ukraine is providing further momentum to the trend of decentralised production. The rapidly rising costs for transportation as a direct outcome of the oil and gas crisis in the wake of the invasion will further disincentivise travel—both locally to the office as well as regionally and globally. The alternative is a further adoption of video conference technology and the introduction of more integrated production systems that can readily assemble an otherwise dispersed workforce. This will require more investment into broadband technologies, 5G telephone systems, data centres and home IT technology.

4.4.3. Transport

While general mobility has been subdued since the beginning of the COVID-19 pandemic, the Russian invasion will further delay, if not entirely prevent, a return to pre-COVID levels. According to Google, the workplace mobility during the week to 21 March 2022 was 22% below pre-COVID levels. In Germany it was -14%, in France -12% and in the UK -27%. Retail and recreation mobility, i.e. mobility for places such as restaurants, cafés, shopping centres, theme parks, museums, libraries and cinemas, was down significantly as well: -12% in the US, -13% in Germany, -14% in France, and -15% in the UK.§§§§§

As mobility becomes more expensive, the reliance on delivery systems will continue to grow. This is changing the mix of traffic. More and heavier goods vehicles are replacing family cars. The road networks will have to keep pace with the shift in usage.

At the same time, Europe needs to ramp up its liquefied natural gas (LNG) imports if it wants greater independence from Russian gas. The resulting move towards more LNG, which shall come from overseas, will have to be connected to the existing power system. New LNG terminals and the build-out of the supporting transport and regasification infrastructure are necessary.

Experts at the IEA believe that there is some potential to scale up biogas and biomethane supply in the short term even though the lead times for new projects are significant. The technology is low-carbon and offers important medium-term upside for the EU’s domestic gas output. However, also in this area infrastructure investments will be necessary as the biogas has to be transported as well.

5. Key Challenges for Financial Markets

For the further discussion, there are three core assumptions with regard to how the Russian-Ukrainian war will affect financial markets in the longer term:

- Increased volatility

- Challenges to economic growth

- Surge in inflation

5.1. Increase in long-term volatility

As described in earlier chapters, the Russian invasion has triggered a retaliatory response by NATO and its allies of an unprecedented kind, employing a forceful strategy of economic and financial isolation against the aggressor that few observers would have expected. The full ramifications of those actions and the subsequent reactions by Russia are not all clear yet, but they have already added to a higher degree of uncertainty. As the involved actors’ countenance measures and countermeasures, it becomes harder for financial markets to project into the future, which in turn creates more volatility.

From a purely military perspective, the probability of a tail-risk scenario, i.e. the use of nuclear weapons in Europe, just multiplied as the Russian invasion was failing to achieve the desired quick victory. This tail-risk scenario has arguably become more probable than at any time since the fall of the Iron Curtain, with unknown consequences for the world. Even if the Russian-Ukrainian conflict were to end soon and without further escalation, the world realised how precariously close it might have come to see the deployment of nuclear weapons on the battle field, thus creating a lasting effect on military risk analysis for the future. A retrenchment from this scenario would only happen very gradually and over a long period of time.¶¶¶¶¶

As the bombs keep falling in Ukraine, international contracts are being ripped up or unilaterally changed. The US, Europe and other allies refuse Russia access to central bank reserve funds held in their jurisdictions, while Russia seizes foreign assets and declares existing contracts null and void.

For several decades, the level of confidence in international treaties and contracts—be they between nations or between companies of different nations—has been rather high by historic standards and reinforced by a series of international institutions, such as the WTO. However, the Russian conflict has undermined this confidence and going forward investors will have to take into account that economic sanctions and financial measures happen faster and become more painful than during the previous era.

As the world is retreating more within national borders and striving for more autonomy, it will also place less weight on international treaties since they are seen as less binding and thus becoming slightly less relevant for the functioning of a nation. While more interdependence among nations was meant to create more stability, less interdependence is very likely to lead to the contrary. And less political stability means more financial volatility.

5.2. Growth Challenges

There are some very obvious consequences that stem directly from the current conflict in Eastern Europe and which have an impact on economic growth:

- The war is costing Russia and Ukraine billions of dollars in military expenditure.

- The allies who are supporting Ukraine’s defence effort, are also spending billions providing weapons, logistical and economic support.

- Russia and Ukraine are destroying important parts of the European infrastructure, which have to be rebuilt.

- They created additional costs for other nations, especially NATO, who responded by moving military personnel and equipment, adjusting their defensive capabilities.

- They triggered rearmament around them.******

- In Ukraine, the war has devastated large parts of the economy already

- The economic and financial sanctions implemented will lead to a deep recession in Russia

- Energy and commodity prices, especially those provided by Russia, surged.

- International companies are leaving the Russian market and future direct investments are curtailed

- Supply chains are being rerouted

- Millions of citizens have left their homes and jobs and are resettling elsewhere

- The IT infrastructures of various countries were attacked

- A further escalation of the energy delivery stand-off between Russia and the EU carries the risk of a European recession

All the above have a negative impact on growth: very significant in the short term but in many cases reducing growth prospects in the longer term as well. A new phase of stagflation has become much more likely. The negative supply shock, coupled with a wider adjustment to the new security landscape, is expected to create higher prices in the absence of meaningful growth.

However, there is an additional element to take into account. The Western retaliation to the Russian invasion was to freeze Russia out of the global financial system. The lessons for nations not dealing in US dollars or Euros is twofold: First, when foreign currency reserves can be frozen so readily—as happened to the Russian assets held at the central banks in the US, EU, Japan, UK, Canada, Australia and Switzerland—then the value of those assets is far less relevant than in the past. As a consequence, other nations will build them less and use them less. Second, when payment systems and banking networks can cut off a nation’s financial infrastructure, then that nation—and others like it—will design alternative strategies. It seems that the participation of the countries of the world in American and European designed and dominated financial infrastructures will be considerably lower in the future. This means that transaction costs, which gradually declined as part of the globalisation process, will rise again, thus also dampening future growth.

5.3. Surge in Inflation

For many years, inflation in the developed world was more of academic interest than a real business concern. As central bankers watched over inflation developments, the era of globalisation and especially the integration of China into the world economy on a large scale, led to a period of sustained low inflation.

Immediately following the Russian invasion, markets reacted by sharply pushing energy prices up: crude oil is almost 80% dearer year-on-year, gas more than 100%. Other commodity prices have moved sharply upwards as well: lithium over 250% (year-on-year), magnesium 150%, nickel 100%, tin and cobalt over 60% while oat, cotton, coffee, wheat and palm oil are up by between 60 and 80%.††††††

As energy becomes more expensive, so will the goods that further downstream depend on energy. The inflationary shock to the system has already started to create secondary waves and it is likely that those will not only multiply but are likely to become more pervasive and entrenched. Inflation feeds to a certain degree on itself as it pushes everybody’s expectations upwards, thus creating an environment where it can become self-fulfilling. In a low-growth environment, as discussed above, the tools for governments and central banks to combat inflation are severely restricted.

For investors this means that they need to adapt their strategies. Asset classes that provide direct or indirect inflation protection are likely to outgrow those that do not. It will be hard to make a case for bonds in such a scenario and even inflation linkers have their limitations as adverse movement in spreads could frustrate the investment goal.

Overall, it is expected that manufacturers and consumers alike will test their pricing power in the new economy. While most experts expect a period of higher inflation, it is less clear for how long this will last. Monetary policy could yet help dampen it and the adjustments to the production systems might bring more growth faster than we currently think.

At the same time, inflation will not be uniform as certain sectors can pass on costs more readily to the market while others cannot. Equally, the impact on wage growth is going to be diverse from one sector to the next. Specialists in those areas that are growing and those sectors that are most relevant to the adaptation process will see their income prospects rise.

6. Final Reflections

When Herbert George Wells wrote in 1914 about World War I that it would be “the war to end all wars”,‡‡‡‡‡‡ it was idealistically perceived as being the entry point to a new era of peace. However, as it turned out, it was the aftermath of World War I that should directly contribute to World War II, as too many questions remained unstable and problems among nations not only unresolved but exacerbated. It was only after World War II and ironically with the emergence of the stalemate between the US and the USSR as dominating world powers with rivalling ideologies that ushered in a period of stability and economic growth, especially for Europe.

The last decade of the 20th century and the beginning of the 21st saw an acceleration of the trend to connect nations more intimately with each other. The participation in a modern intertwined production and consumption networks allowed more countries to participate and reap the benefits of global co-operation. Greater cultural exchange ensued as well and thus globalisation was born, resulting in more economic growth and wealth creation worldwide.

However, as we posit in this paper, we see strong indicators that the Russian-Ukraine conflict marks the end of this period of relative stability, (relatively) low global military spending, and wide-spread international co-operation. Of course, even during the past three decades, the inevitable conflicts arose from time to time, but usually they remained localised events that never seriously called into question the overall trend towards ever more globalisation.

This is now changing as nations have begun to entrench and decouple in search for greater independence and autonomy. National security and questions of sovereignty are moving up the list of priorities.§§§§§§ The key question for everybody on this planet is, what will come next?

The answer to this question should be in our hands. A phase of de-globalisation does not per se have to be bad. It is likely that the coming years will see smaller economic advancements for individuals as the peace dividend and the benefits of accelerating globalisation are disappearing while the frictional cost (military spending, near-shoring expenses, border and transit complications etc.) are rising again. However, this phase could be used to address the vulnerabilities that have built up in the relations among nations. The new world order is not set and even though many expect a similar duopoly to emerge between US and China, thus replacing the US-USSR duopoly of old, this is not a forgone conclusion and history hardly ever repeats itself in the same way.

One thing seems certain though, after more than 10 weeks into the Russian-Ukraine conflict: Following this war, Russia will have to come to terms with the harsh reality of being no more a top tier power in the world—nuclear weapons alone do not justify such a standing. Given the direct and especially the indirect cost of the confrontation, Russia will fall economically even further behind the US, China, India, Brazil and the leading European nations. Geopolitically, it will have a reduced sphere of influence, particularly as previously neutral nations in Central and Eastern Europe (such as Finland, Sweden, Switzerland or Austria) are realigning themselves while Russia’s neighbours (such as Poland, Romania, Bulgaria as well as the Baltic states) are detaching themselves further, too.

Russia will have to determine whether it wants to continue antagonising Europe, where it has its traditional historic ties, as well as the US and other NATO states. The consequence would likely be a drift towards becoming a vassal to an economic and militarily far superior China. But maybe Russia can find a role again as a dependable international partner that ideally excludes or at least significantly reduces military aggression from the list of acceptable policy options. This might be hard to imagine under the current leadership. However, the same would have applied to Germany and Italy in the early 1940s. And while “Change through trade” might have been the wrong formula for dealing with an autocratic regime, it might be an option if and when Russia decides to become a real and sustained democracy. The world, especially Europe and the US, should have an interest in helping Russia on this way rather than writing the nation off completely.

Bibliography

- Chad Bown, (2022): “The US-China Trade War and Phase One Agreement”, Peterson Institute for International Economics, www.piie.com/sites/default/files/documents/wp21-2.pdf

- CEPII (2022): CEPII database for 2020, visualised as per OEC, http://www.cepii.fr

- European Commission (2022), ec.europa.eu/commission/presscorner/detail/en/ip_22_1511

- European Commission (2022), ec.europa.eu/info/topics/energy_en

- European Commission (2022), IEA press conference on 3 March, 2022 ec.europa.eu/commission/commissioners/2019-2024/simson/announcements/remarks-commissioner-simson-iea-press-conference-its-10-point-plan-reduce-european-unions-reliance_en

- European Parliament (2009), Resolution of 5 February 2009 on Trade and economic relations with China (2008/2171(INI)), www.europarl.europa.eu/doceo/document/TA-6-2009-0053_EN.pdf

- IEA (2022), “A 10-point plan to cut oil use”, www.iea.org/reports/a-10-point-plan-to-cut-oil-use, accessed on 29 March 2022

- IEA (2022), www.iea.org/articles/frequently-asked-questions-on-energy-security

- IEA (International Energy Agency) (2022), www.iea.org/reports/russian-fossil-fuel-reliance-data-explorer

- IMF (International Monetary Fund) (2022), IMF data, www.imf.org/en/Data

- Jade Lee & Eugene Wong, (2021). Suez Canal blockage: an analysis of legal impact, risks and liabilities to the global supply chain.

- Sauli Niinistö (2022): Press Release by the office of the Finnish president, https://www.presidentti.fi/en/press-release/president-niinisto-spoke-with-russian-president-putin-6/

- Reuters (2022), https://www.reuters.com/world/china/exclusive-biden-sends-former-top-defense-officials-taiwan-show-support-2022-02-28/

- Russian Federation (2022): Customs Statistic of Foreign Trade of Russia as per http://stat.customs.ru/

- Olaf Scholz, on 27 February 2022. As per www.bundesregierung.de/breg-en/news/policy-statement-by-olaf-scholz-chancellor-of-the-federal-republic-of-germany-and-member-of-the-german-bundestag-27-february-2022-in-berlin-2008378

- Trade data monitor (2022), tradedatamonitor.com/index.php/data-news-articles/145-gold-oil-diamonds-and-fertilizers-10-things-you-need-to-know-about-russian-exports

- UN (2022), UN General Assembly, news.un.org/en/story/2022/03/1113152

- USGS (2022), USGS data as per pubs.er.usgs.gov

- Washington Post (2022), “War in Ukraine generates interest in nuclear energy, despite danger”, https://www.washingtonpost.com/climate-environment/2022/04/15/nuclear-energy-europe-ukraine-war/

- Wells, H.G. (1914), The War That Will End War.

- World Bank Data (2022), wits.worldbank.org/CountryProfile/en/RUS

- World Bank Data (2022): data.worldbank.org/indicator/NE.TRD.GNFS.ZS?end=2020&start=1970

* Source: IMF data as per www.imf.org/en/Data, accessed on 29 March 2022.

† Source: World Bank Data as per data.worldbank.org/indicator/NE.TRD.GNFS.ZS?end=2020&start=1970, accessed on 25 March 2022.

‡ While the global coronavirus (SARS-CoV-2) pandemic saw a sharp drop in 2020 in global trade as percentage of GDP, which stood in 2019 at 56.3%, it is notable that the growth trend had been broken in 2008, for every year since then has been lower than the peak value of 61%.

§ Indeed, FDI grew steadily during the 1990s and then suffered two periods of set-backs, from 2001 to 2003 in the aftermath of September 11 and the dot-com stock crisis, and then again from 2008 to 2009 as a consequence of the Global Financial Crisis. However, FDI grew fast after these periods making up lost ground fairly rapidly and reverting back to an upwards growth trend. It has only been in recent years that the long-term growth trend was broken.

¶ See e.g. the speech of Federal Chancellor Olaf Scholz of 27 February 2022 in the German Parliament that was widely seen as a total re-write of Germany’s post-war foreign and defence policy: www.bundesregierung.de/breg-en/news/policy-statement-by-olaf-scholz-chancellor-of-the-federal-republic-of-germany-and-member-of-the-german-bundestag-27-february-2022-in-berlin-2008378 accessed on 5 May 2022.

** On 28 February 2022, the US sent a delegation to Taiwan led by former Joint Chiefs of Staff Chairman Mike Mullen amid fears Beijing could invade the island during Ukraine crisis. See https://www.reuters.com/world/china/exclusive-biden-sends-former-top-defense-officials-taiwan-show-support-2022-02-28/, accessed on 28 April 2022.

†† On 14 May 2022, Finnish President Sauli Niinistö told President Putin how fundamentally the Russian demands in late 2021 aiming at preventing countries from joining NATO and Russia’s massive invasion of Ukraine in February 2022 have altered the security environment of Finland. President Niinistö announced that Finland decides to seek NATO membership in the next few days. https://www.presidentti.fi/en/press-release/president-niinisto-spoke-with-russian-president-putin-6/ accessed on 15 May 2022.

‡‡ We shall discuss this in more detail later in this paper.

§§ The IEA (International Energy Agency) writes on its website that “In 2021, more than half of Russia’s oil exports went to Europe, which received about one-third of its oil imports from Russia. Germany was the largest European buyer of Russian oil, followed by the Netherlands and Poland.” www.iea.org/articles/frequently-asked-questions-on-energy-security accessed on 9 May 2022.

¶¶ ec.europa.eu/commission/presscorner/detail/en/ip_22_1511, accessed on 29 March 2022.

*** European Parliament Resolution of 5 February 2009 on Trade and economic relations with China (2008/2171(INI)) www.europarl.europa.eu/doceo/document/TA-6-2009-0053_EN.pdf accessed on 29 March 2009.

††† For a deeper analysis of the 2017 to 2021 trade war between the US and China see e.g. Chad Bown’s paper “The US-China Trade War and Phase One Agreement”, published by the Peterson Institute for International Economics, www.piie.com/sites/default/files/documents/wp21-2.pdf

‡‡‡ Last available data for 2019 wits.worldbank.org/CountryProfile/en/RUS accessed on 29 March 2022.

§§§ Using the CEPII database for 2019, visualised as per OEC.

¶¶¶ www.iea.org/reports/russian-fossil-fuel-reliance-data-explorer accessed on 29 March 2022. A value of 100% could actually also mean that more Russian oil was imported than used during the year by the country in question.

**** USGS data as per pubs.er.usgs.gov, accessed on 29 March 2022.

†††† Cited from tradedatamonitor.com/index.php/data-news-articles/145-gold-oil-diamonds-and-fertilizers-10-things-you-need-to-know-about-russian-exports, accessed on 29 March 2022.

‡‡‡‡ For a more detailed analysis see Lee, Jade & Wong, Eugene. (2021). Suez Canal blockage: an analysis of legal impact, risks and liabilities to the global supply chain.

§§§§ The UN General Assembly overwhelmingly adopted a resolution on 2 March 2022, demanding that Russia immediately end its military operations in Ukraine. A total of 141 countries voted in favour of the resolution, which reaffirms Ukrainian sovereignty, independence and territorial integrity. Only 5 voted against. See news.un.org/en/story/2022/03/1113152, accessed on 29 March 2022.

¶¶¶¶ “The European Commission is committed to policies that will contribute to the European Green Deal ambition of achieving carbon-neutrality by 2050. They are also aimed at boosting the internal energy market, making our energy more secure, more sustainable and more affordable.” See ec.europa.eu/info/topics/energy_en, accessed on 29 March 2022.

***** Remarks by Commissioner Simson at the IEA press conference on 3 March, as per ec.europa.eu/commission/commissioners/2019-2024/simson/announcements/remarks-commissioner-simson-iea-press-conference-its-10-point-plan-reduce-european-unions-reliance_en, accessed on 29 March 2022

††††† See e.g. reporting by the Washington Post as per https://www.washingtonpost.com/climate-environment/2022/04/15/nuclear-energy-europe-ukraine-war/ accessed on 5 May 2022.

‡‡‡‡‡ See www.iea.org/reports/a-10-point-plan-to-cut-oil-use, accessed on 29 March 2022

§§§§§ As per https://www.google.com/covid19/mobility, accessed on 25 March 2022.

¶¶¶¶¶ Note: The closest historic parallel that is being drawn up is the Cuban missile crisis of 1962, which very nearly ended in the deployment of nuclear weapons and shaped security thinking for decades to come.

****** The most visible example being Germany’s decision to ramp up defence spending by EUR 100bn and committing to keeping it above 2% of GDP in the future. See the earlier mentioned speech by German Federal Chancellor Olaf Scholz on 27 February 2022. As per www.bundesregierung.de/breg-en/news/policy-statement-by-olaf-scholz-chancellor-of-the-federal-republic-of-germany-and-member-of-the-german-bundestag-27-february-2022-in-berlin-2008378, accessed on 5 May 2022

†††††† Data as per Bloomberg and Reuters, accessed on 29 March 2022.

‡‡‡‡‡‡ H. G. Wells (1914): The War That Will End War. Note: The quote “the war to end all wars” is the more modern and popularized version of the originally used “the war to end wars” by the author.

§§§§§§ See e.g. the UK’s (Br)exit from the EU, where a small degree in additional sovereignty was acquired at the price of significant economic disruption, lower growth, higher inflation and the reversal of a decade-long trend towards more European integration.

About the Author(s)

|

Patrick Liedtke Fellow, World Academy of Art and Science; Visiting Professor for Risk and Insurance, Bayes Business School, City University London, England |